CSRD data management and reporting

1. Select the material topics based on the DMA for your CSRD report

2. Create a reporting template in three seconds

3. Define your group structure

4. Gather data automatically with data request function or API with automatic consolidation and unit conversion for data

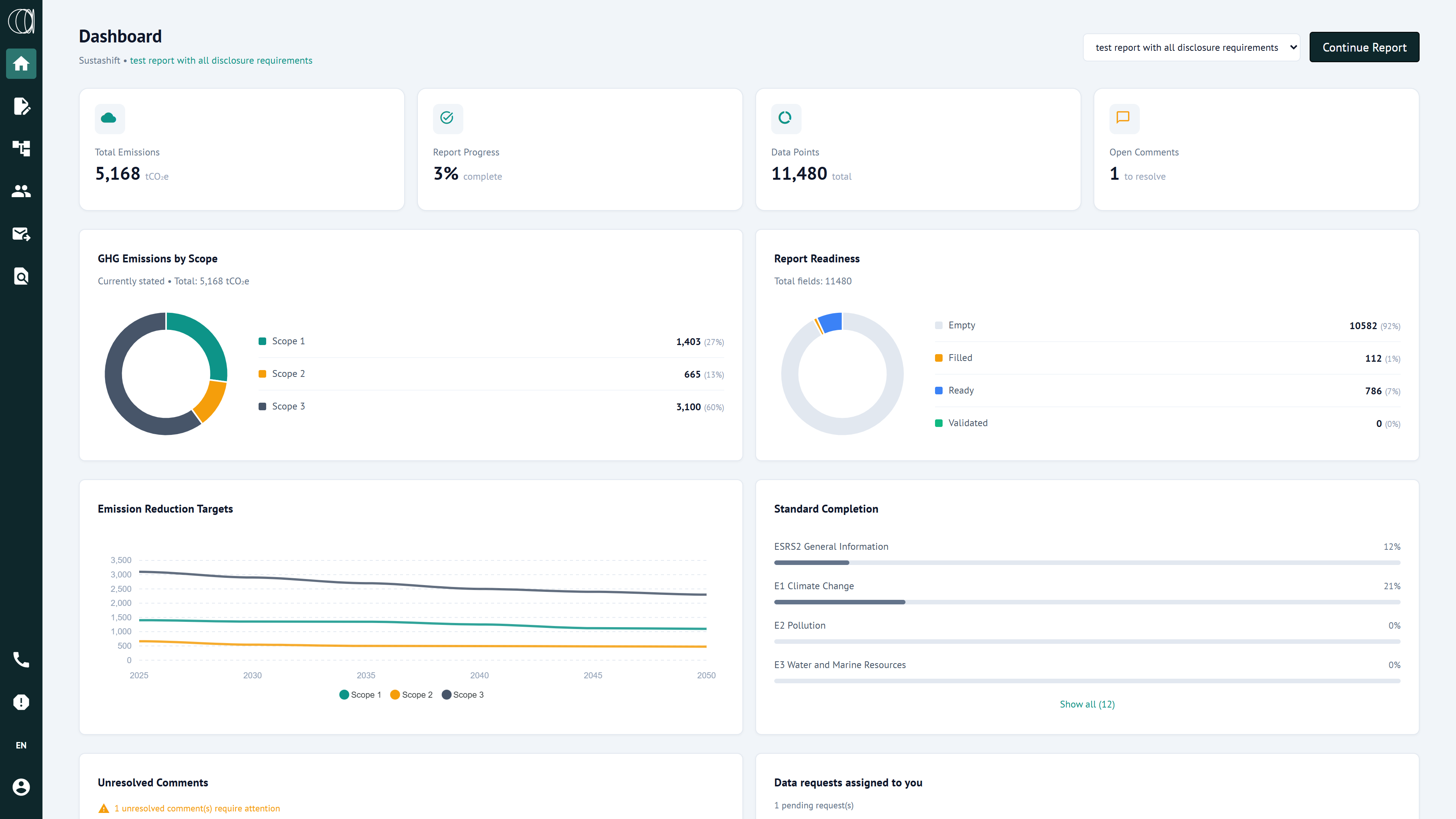

5. Add all required users, define tasks and timelines and track the progress of reporting

6. Create your publish ready final report - with XBRL tagging in 5 seconds

Define disclosure requirements

Choose the disclosure requirements that are relevant for your company according to the results of your double materiality assessment. We will make sure that mandatory requirements are automatically chosen, so you won’t make any unneccesarry mistakes.

A ready-made Model Document

Based on the relevant disclosure requirements, model documents are created automatically which ensures compliance with the ESRS standard. Model documents contain all MDR, DR and AR requirements combined to a single easy to fill form.

.png)

Plan and simulate climate transition plan and required actions and their effects

Choose the disclosure requirements that are relevant for your company according to the results of your double materiality assessment. We will make sure that mandatory requirements are already chosen, so you won’t make any unneccesarry mistakes.

Co-operate with your team and auditor to streamline the CSRD reporting process

Leave comments and verify the information in your report among your team members. When your report is ready for auditing, click the ready for audit button and your auditor will be granted viewing access and a commenting function, streamlining the auditing process and reducing costs.

Assign tasks and timelines for your team members and follow progress to ensure adhering to project schedule

CSRD reporting process involves people from all parts of your organization. Assigning tasks and timelines ensures that everyone has delivered their part on time creating a seamless reporting process which makes sure that your reporting stays on schedule.

No need to tag each requirement—we’ve done it for you

Automatic XBRL tagging significantly reduces the time required for regulatory reporting, saving up to 500 hours of manual work.

Mark the Requirements as Ready for Auditing

The auditor will receive the content and can leave comments so that you can modify. No need to have 5000 versions.

Export report upon auditor approval

We’ll also allow you to export the report in Word format, in case you want to make some visual changes before submitting.

.jpg)

FAQ

How is the auditing done?

C-Tag contains an integrated audit function, where the auditors are added to the platform and they can audit the report datapoint by datapoint. They always have access to the requirement, disclosure and relevant source. The tool keeps an audit trail and creates an audit trail report on request.

Can I assign tasks and timelines in the tool to my team?

Yes, you can assign certain tasks to be completed by your team members and set a timeline. You can follow the reporting process and follow real time the creation of your compliant CSRD-report.

Does C-Tag help with ESRS compliance?

C-Tag contains all ESRS requirements in ready-to-use model documents. When you fill in the empty boxes, the CSRD-report is complete.

How long does XBRL-tagging take with C-Tag?

Tagging takes 3-8 seconds and is done without errors every time. With manual tagging solutions the tagging takes 500 hours.

Do you offer advisory services for writing the CSRD report?

Yes, we have a team of advisors ready to write your CSRD reports in English or Finnish.

If we have used another advisor for our Double Materiality Assessment, can we still use C-Tag for CSRD reporting?

Yes, you can just tick the boxes in our C-Tag software based on your external DMA assessment result and you are ready to start writing your CSRD report.

Do you offer a solution for Double Materiality Assessment?

We offer a double materiality assessment solution and a turnkey DMA assessment as a service.

Which language versions do you support?

We support English, German, Swedish and Finnish languages with additional languages coming in 2025.

Are software updates included in the license?

General software updates are included in the license fee, however company specific additional requests may require additional costs.

What does the C-Tag annual price include?

The price includes the annual usage of the software for up to 50 users and an initial setup and introduction session with the client. The software contains all ESRS requirements in pre-made model documents, integrated data gathering and management, reporting project management and auditing functions. Pricing is dependent on the size of the company.

How can we help?

Contact us

Contact regional sales